The Crypto Bubble Endgame

In January, I wrote an unpublished article detailing the Terra ecosystem, the fragility of UST, and how a de-peg might spread to the rest of crypto.

Below is an article I wrote in January 2022 about Terra and the systemic danger it posed to the rest of the crypto ecosystem. It is pasted below in its entirety, with slight modifications for clarity. Beneath it is an additional addendum, given the events of the last week. Given the UST de-peg this week and its corresponding fallout, I hope that it can offer some insight into how such a collapse could have been foreseen—and perhaps, in the future, avoided.

The game of musical chairs is coming to a close soon, and here’s how it will happen.

It’s an open secret that the DeFi boom of 2020-2022 has been propped up by self-referential financial engineering schemes. Participants regularly self-identify as “degens” participating in “Ponzis”, “yolo”ing into and “shilling” “shitcoins” hoping their “bags will pump.” Some celebrate the absurdity of the system with a knowing wink and nod, but even for them, underneath the starry-eyed dreams of an egalitarian, democratized, Web3 future, there is the sober understanding that this is, in fact, a bubble, and shall also pass: the bubble will pop, prices will decline, and chumps will be left “holding the bag”.

For most participants (speculators and “buidlers” alike), this will be the end of their involvement in the crypto ecosystem. For my part, I still believe in the idea of a “productive” asset bubble, and that crypto can still fundamentally be a force for good. The last few crypto bubbles (2017 and 2020-2022) were not tulip, sardine, or real estate bubbles; they are more like railroad or dot-com bubbles, in which financial excess subsidized the R&D of invaluable infrastructure for the future. But, long-term optimism aside, there is no question that storm clouds are gathering on the short-term horizon. How and when exactly the great reckoning will happen is not well-understood.

Below, I will describe in detail a few crypto protocols of systemic importance (the stablecoin protocol Terra and its ecosystem, the stablecoin money market protocol Curve Finance, and selected lending protocols). Using these “parts” as representatives of the “whole”, I hope to identify a set of self-reinforcing cycles which exist in the crypto ecosystem—which heretofore exist as virtuous cycles, but will soon turn vicious. I will offer some hypotheses for how the vicious cycles will begin, and what that will mean for venture capital investing. While primarily a “macro” speculation, I believe the consequences will have lasting impact on the sorts of entrepreneurs and businesses that will emerge in the next few years.

DeFi’s Self-Referential Debt

The Macro Statistics

The current crypto bubble is a classic debt bubble insofar as it involves the rapid expansion of leverage and novel financial products which transfer and obscure risk. Qualitatively, it is also a textbook bubble in that prices are high relative to traditional measures, market participants are bullish and discounting universalist narratives of Web3 expansion, and new buyers (retail and institutional alike) have entered the market to make exceptionally leveraged speculative investments [Dalio].

Therefore, like with the 2008 crisis, the key to understanding the DeFi ecosystem is to understand the ways in which debt is created, moved around, and subsequently obscured. To give a broad sense of of the scale of debt in the ecosystem today, consider the following:

VC funding reached a record of $33B deployed to crypto startups in 2021 [Galaxy Digital].

Futures interest aggregated across centralized exchanges is just short of $20B as of this writing [TheBlock].

Total stablecoin supply is at $150B. We will come back to the role of stablecoins in the bubble.

Finally, there is around $215B of “total value locked” (TVL). TVL is a measure of crypto “locked” or “staked” in protocols to earn returns or show support for a project.

All of this is just to show the truly global proportions that crypto has reached in the last two years. Let’s double-click a bit on the TVL figure above to understand some of the systemic risks that exist on-chain.

The Unit of Account: Stablecoins and the Terra Ecosystem

Below, I describe some of the highest TVL protocols and their interrelations. As of this writing, they include: Curve (#1 with $21.5B), Convex (#2 at $16.35B), Maker (#3 at $15.5B), Lido (#6 at $9.7B), and Anchor (#8 at $9B) [DeFiLlama].

Terra, Anchor, and Lido

Terra is a stablecoin protocol and its own L1 blockchain. While not the largest stablecoin in terms of market share (trailing Tether, USDC, Dai, and Binance USD), it is still systemically important for reasons to become clear shortly. At a high level, as of this writing, it has ~$17B in TVL in its ecosystem [DeFiLlama].

Terra is made up of two tokens: Terra stablecoins which are pegged to fiat currencies (currently, the dollar via TerraUSD or “UST”) and Luna, the native staking token which is meant to absorb the volatility of Terra. Simply, the supply of Luna expands and contracts in order to defend the UST peg. Therefore, when UST is trading below the peg, arbitrageurs will burn <=$1 of UST for ~$1 Luna; when UST is above, arbitrageurs will burn Luna to issue new UST. The price of Luna has appreciated from $0.90 to $70 in the last year, presumably driven by demand for UST. Where does UST demand come from?

Anchor is a savings protocol built on the Terra blockchain and its #1 protocol by TVL (at $9B). It promises savers a stable 19-20% return on their Terra USD deposits, and has largely kept its promise so far.

How does it promise such an attractive return with no risk? First, it is an overcollateralized lending market with dynamics similar to Maker, Compound, and Aave: borrowers stake assets as collateral and pay interest (which fluctuates according to supply and demand) and are liquidated when their maintenance margin dips below the required ratio. The innovation which Anchor offers is that, unlike with other lending protocols, users use proof-of-stake assets as collateral. Recall that in proof-of-stake consensus, users can stake their assets to secure the network and earn block rewards. Therefore, Anchor supplements and stabilizes the rate paid by borrowers with the block reward earned by staking in proof-of-stake blockchains [whitepaper]. Anchor supports ETH and Luna (Terra blockchain) as collateral.

If the interest payment and the block reward do not add up to the promised 19-20%, then Anchor will pay out of its reserves. Those reserves are set to run out by the end of February [MirrorTracker].

Finally, in order to actually borrow on Anchor, you have to first stake your ETH (or Luna or SOL) with Lido Finance, which creates “stETH” or “staked ETH”, which you can then use in Anchor as “bETH” or “bonded ETH” or “bLUNA”.

In order to incentivize borrowing, both Lido and Anchor are offering “rewards”, which subsidize borrowing. For Anchor, you are paid ~4% to borrow UST (which you can then turn around and deposit on Anchor for 19%).

The virtuous / vicious cycle should be becoming clearer by this point. We will flesh it out in detail in a later section. For now, we move onto other interrelated protocols.

The Money Markets: Yield Farming

Curve Finance is the largest non-L1 protocol in the cryptocurrency ecosystem. It is the “money market” in that it is the emergent Schelling point where users deposit their stable (e.g., stablecoins) and blue-chip tokens (ETH, BTC) to earn a return. Curve generates fees from and offers some of the lowest fees for stablecoin-to-stablecoin swaps.

Why would anyone need to swap two assets which are pegged to the same underlying fiat currency? In the crypto ecosystem there are several different types of synthetic versions of the same assets, and each has slightly different uses. Dai and USDC, for instance, are both USD-equivalents, but Dai has access to a number of savings accounts in the Maker ecosystem and is used to pay gas on the xDai/Gnosis Chain. USDC is used for most trading applications. Similarly, you can use Curve to trade various forms of ETH (stETH to regular ETH) and BTC (BTC, renBTC, and wBTC).

Accordingly, Curve can also be thought of as the primary router through which most protocols inter-operate—hence, its systemic importance. Anchor and Lido both have relevant pools on Curve: there is a UST to stablecoin pool (for UST, the central token for Anchor) and a stETH (which is a Lido construct) to ETH pool.

The Curve Wars

Because of its systemic importance and the massive amount of volume flowing through the exchange, Curve has become embroiled in the center of DAO politics. Rewards for each pool are set through decentralized governance, which means that tokenholders vote on how to allocate rewards. As a result, a number of protocols, with Convex at the forefront, have created applications that build atop Curve with the goal of accumulating CRV governance tokens, locking them up, and centralizing voting power and therefore the rewards [CoinDesk].

Convex Finance (along with Yearn, Cream, and other “runner up” mentions) is a leveraged yield farming protocol. It controls just shy of half of the voting power on Curve Finance. Herein lies another self-reinforcing cycle. Depositors are incentivized to deposit their CRV with Convex because it already has the highest concentration of CRV, and therefore will dictate where the returns from Curve go. The more CRV is “locked” away with yield farming protocols, the more valuable CRV becomes; the more valuable CRV becomes, the more depositors seek rewards by buying CRV and staking it with Convex. On top of this, depositors of CRV on Convex also receive CVX tokens, which are subject to the same virtuous cycle. CRV and CVX were both up around 6x in 2021, presumably due to this dynamic.

Finally, other crypto protocols and DAOs are themselves participants and soldiers alike in the “Curve Wars”, with significant portions of their treasuries held in CVX, for instance [CoinDesk]. See above figure.

The Lending Protocols

Maker: Historical Black Swans

Maker is an overcollateralized lending protocol, and one of the first of its kind, predating protocols like Compound, Aave, and Liquity. Its TVL stands at $14B as of this writing, making it the third most popular DeFi protocol behind Curve and Convex.

Maker functions as the central bank of the ecosystem. This is because, unlike other protocols, it is not a marketplace that matches borrowers and lenders. Rather, the borrower stakes collateral at a predetermined (over)collateralization ratio to produce new Dai stablecoin. They pay an interest rate which is set by decentralized governance (i.e., tokenholders voting). As a result, the Maker interest rate is the “substitute good” which drives rates for the rest of the lending protocols as well. Maker is an interesting system unto itself, but the aspect of Maker which is germane to our analysis is the black swan event that it endured in March 2020.

On March 12 and 13, 2020, a precipitous decline in ETH price forced a number of borrowers below their minimum collateralization ratio, at the same time that the Ethereum network became extremely congested, leading to a sharp rise in gas price. As a result of the high gas (transaction) prices, liquidators stopped liquidating lenders [MakerDAO] and oracles (crucial bits of infrastructure which keep on-chain price feeds up to date) stopped functioning [CoinDesk]. This led to a number of odd things happening at once:

Dai’s price, which is supposed to be 1-for-1 with USD, was temporarily at $1.10 [CoinDesk].

Strangely, at the same time, around $5.7mm DAI was left uncollateralized [Medium].

One liquidator bot was able to take advantage of the situation, and was able to bid ~$0 to gain $4mm of ETH collateral (since there were no other bidders).

The protocol eventually recovered fully (and is actually in better financial health now than ever before [Maker]). But the event had left the community searching for protections against a recurrence.

In response to the event, Maker’s creator began a campaign to add additional, varied collateral to the service. In particular, they voted to allow USDC collateral (at a 110% collateralization ratio, since lowered to 101%) immediately as an emergency measure to restore the $1 peg.

Now, stablecoins make up ~53% of Maker’s collateral. It should go without saying that this represents a unique systemic risk to the use of stablecoins—it’s possible that another “run on the banks” or system malfunction could send stablecoin prices on a nosedive or upswing.

Reflexivity: Self-Reinforcing Cycles

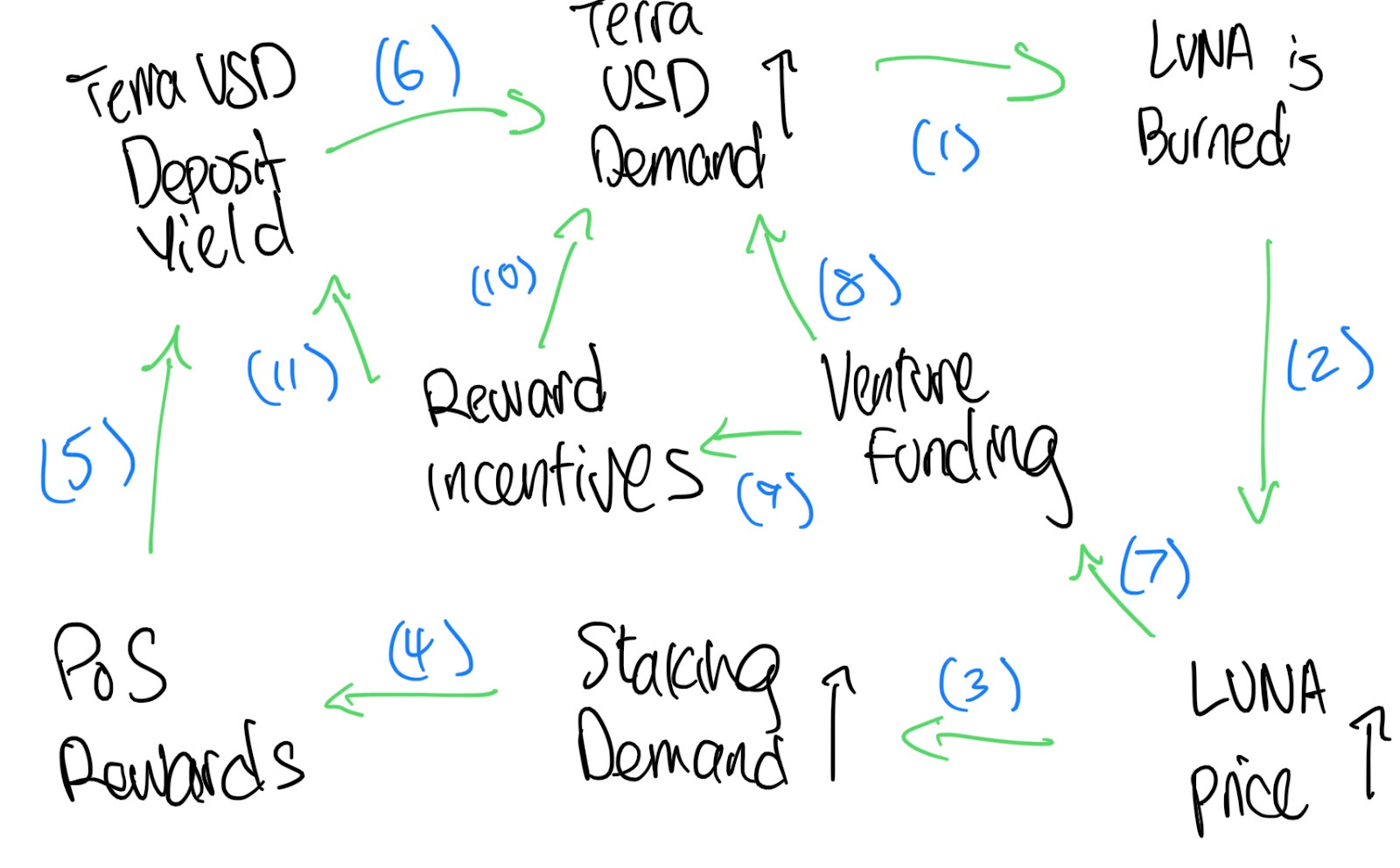

By now, I hope to have made clear two phenomena. First, that the mechanisms governing the expansion of the crypto ecosystem are self-reinforcing. Second, that the protocols themselves are highly interdependent on one another, and therefore systematically correlated. Below, I attempt to sketch a formal concept of the virtuous cycle in the Terra ecosystem, with the intent of using it as an aid to guide an understanding of how it may reverse. Although it is a description of only one protocol (Terra), I believe it is still an illustrative case study because (1) it is sufficiently representative of the dynamics of many other protocols as well and (2) we have shown how Terra is systematically correlated to the rest of the ecosystem via Lido, Curve, and Convex, to name a few.

A brief commentary on the linkages.

Increasing UST demand causes UST to trade above the peg. LUNA must then be burned to mint UST to weaken UST.

This causes LUNA’s price to increase.

LUNA price appreciation incentivizes more staking in the Terra blockchain.

Staking in the Terra blockchain produces PoS rewards which, if the staked asset is deposited in Anchor, is one component of the 20% UST deposit yield.

Consistent proof-of-stake (PoS) rewards drive UST yields.

High UST yields drive UST demand.

Luna price appreciation indirectly stimulates venture demand for Terra ecosystem projects [TechCrunch].

Venture funding drives UST demand as more projects are built that need to use it.

Venture funding also drives reward incentives, which could be used for (10) directly stimulating borrowing or (11) the yield reserve, which props up the deposit yields.

Catalysts for Implosion

Each node represents a point of failure, and it would be beyond the scope of this essay to examine each in depth. We focus our attention on the venture funding environment and regulation as potential causes of systemic contagion.

Venture Funding

Venture funding creates the conditions for reflexivity to take hold. By funding “ecosystems”, venture investors pump prices and drive “fundamental” activity vis-a-vis (apparent) usage of the protocols. Of course, skyrocketing prices then influence the fundamentals further in the ways described above (by incentivizing activity and staking).

Venture funding is an exogenous force, so it is easier to distinguish cause from effect. Especially now as the Fed is raising rates and tightening QE to combat inflation, long-duration and “risk-on” assets have been in decline. In the short-term, this has already had an impact on crypto prices. In the medium-term, it also means that LPs will begin to allocate less to tech, growth, and venture asset classes as yields compress and returns disappoint. This will mean fewer rewards to incentivize the financial engineering schemes of protocols like Anchor.

However, I suspect that the pullback in financial activity attributable to declining venture funding will not begin for some time. The venture capital institutions are themselves aware of the macroeconomic environment, and have accordingly raised fresh funds in recent months. These funds will likely continue to prop up cryptocurrency prices and activity in the short- to medium-term, though against the headwind of macro-driven outflows.

I do not think that there will be significant LP appetite for more crypto funds into 2022 and 2023 as risk-on asset prices decline. If I am correct, then the drying up of venture funding will remove the primary support to the 20% “risk free” yield regimes like Anchor’s, precipitating a vicious cycle which begins in one protocol and spreads to others. Concretely, this could look like a precipitous decline in Luna or a broken UST peg. A broken peg would itself spread to other markets via Curve Finance, and cause instability in other cryptocurrency markets.

Regulation

Admittedly, I know less about the latest attitudes and developments from Capitol Hill on stablecoins. If Senator Elizabeth Warren is to have her way, and stablecoins are more heavily regulated or scrutinized, then, per the diagram above, demand for unregulated stablecoins like could decline precipitously. This would put pressure on the peg and force Terra to mint more Luna, driving prices down. From there, as we have discussed, leveraged exposures across multiple protocols would follow suit.

As another hypothetical scenario: USDC is centrally managed, and its smart contracts contain provisions for administrators to freeze token transfers. If for some reason regulators ordered Circle and Coinbase to freeze USDC, then several parts of DeFi (via, e.g., Curve Finance and Maker above) would likely be frozen alongside it, causing a panic.

Conclusions

I’ve now shown a number of plausible scenarios for how the cryptocurrency bubble will end—that is, how the virtuous cycles driving its meteoric growth in recent years could reverse. Below, I describe the ways in which the vicious cycle will affect venture capital investing and companybuilding. Below are a few (very broad) predictions:

Stablecoins won’t be so stable, and businesses which depend on stablecoins and their yields will need to bake this risk into their strategy, or build their own solutions which avoid systemic correlation with other stablecoins.

Crypto fund returns will be lower, as a consequence of high valuations coming down, and also because token ICOs and IDOs (initial DEX offerings) will no longer be an easy way for venture firms to skirt regulation and get liquidity on their investments. This will cause fairweather entrepreneurs and investors to disappear.

There will be a reversion to core infrastructure development, rather than protocols and applications. This is because protocols and applications to date have primarily relied on yield farming schemes to bootstrap initial interest and usage. If that mechanism ceases to be effective, then operators will likely have to (a) focus on harder, technical problems which do not readily admit to tokenomic schemes; these may include zero-knowledge scalability tools, blockchain interoperability, and cross-chain security, and (b) capture value in more traditional “Web2”-reminiscent ways.

May 2022 postscript. Today, Terra is no longer. As of this writing, UST is at $0.20 on the dollar, and LUNA has fallen asymptotically to zero. The Terra blockchain has halted. Fortunes and life savings have been lost.

Crypto is down for the count, but I still believe in its technological merit, and the innovative good it could bring to the world. In retrospect, I think that the lesson here for true builders in crypto is twofold. First, the economic security (at the core consensus mechanism level) of a proof-of-stake blockchain is not simply a theoretical concern, but directly impacted by the chain’s marketing and storytelling. Eventually, when LUNA fell under $100M market cap, the Terra developers had to halt the blockchain due to security concerns around PoS consensus—it would have been possible to mount an attack by buying up the LUNA supply. Second, and more importantly, if my analysis above about the “self-referential” characteristic of Terra’s value chain is correct, then crypto builders ought to re-orient toward “real ” rather than “financial” value creation—that is, products which derive their value from real-world usage, tied to non-financial, non-speculative activities, rather than yield products whose value is undergirded only by the existence of token-buyers in abundance. Perhaps with such a reorientation, crypto will be able to deploy its impressive technological developments toward better ends.